COSO Internal Control Integrated Framework

In 1992, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) developed a model for evaluating internal controls. This model has been adopted as the generally accepted framework for internal control and is widely recognized as the definitive standard against which organizations measure the effectiveness of their systems of internal control.

The COSO model defines internal control as “a process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance of the achievement of objectives in the following categories:

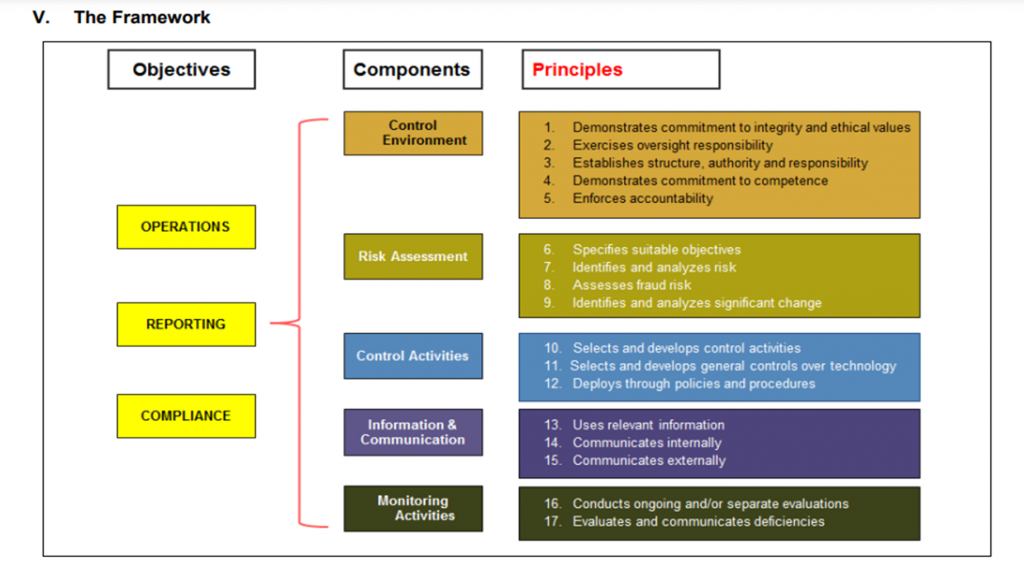

- Effectiveness and efficiency of operations

- Reliability of financial reporting

- Compliance with applicable laws and regulations”

Five Framework Components of COSO

The COSO internal control framework consists of five interrelated components derived from the way management runs a business. According to COSO, these components provide an effective framework for describing and analyzing the internal control system implemented in an organization as required by financial regulations (see Securities Exchange Act of 1934) The five components are the following:

Control environment: The control environment sets the tone of an organization, influencing the control consciousness of its people. It is the foundation for all other components of internal control, providing discipline and structure. Control environment factors include the integrity, ethical values, management’s operating style, delegation of authority systems, as well as the processes for managing and developing people in the organization.

Risk assessment: Every entity faces a variety of risks from external and internal sources that must be assessed. A precondition to risk assessment is establishment of objectives and thus risk assessment is the identification and analysis of relevant risks to the achievement of assigned objectives. Risk assessment is a prerequisite for determining how the risks should be managed.

Control activities: Control activities are the policies and procedures that help ensure management directives are carried out. They help ensure that necessary actions are taken to address the risks that may hinder the achievement of the entity’s objectives. Control activities occur throughout the organization, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications, reconciliations, reviews of operating performance, security of assets and segregation of duties.

Information and communication: Information systems play a key role in internal control systems as they produce reports, including operational, financial and compliance-related information, that make it possible to run and control the business. In a broader sense, effective communication must ensure information flows down, across and up the organization. For example, formalized procedures exist for people to report suspected fraud. Effective communication should also be ensured with external parties, such as customers, suppliers, regulators and shareholders about related policy positions.

Monitoring: Internal control systems need to be monitored—a process that assesses the quality of the system’s performance over time. This is accomplished through ongoing monitoring activities or separate evaluations. Internal control deficiencies detected through these monitoring activities should be reported upstream and corrective actions should be taken to ensure continuous improvement of the system.

17 Principles

Principles are fundamental concepts associated with components. As such, the Framework views the seventeen principles as suitable to all entities.

The Framework presumes that principles are relevant. If management decides that a principle is not relevant, management must support that determination, including the rationale of how, in the absence of that principle, the associated component could be present and functioning. When a relevant principle is deemed not to be present and functioning, a major deficiency exists in the system of internal control. However, a principle being present and functioning does not imply that the organization strives for the highest level of performance in applying that particular principle. Rather, management exercises judgment in balancing the cost and benefit of designing, implementing, and conducting internal control

77 points of fucus.

The Framework describes points of focus that are typically important characteristics of principles. Points of focus assist management in designing, implementing, and conducting internal control and in assessing whether the relevant principles are, in fact, present and functioning.

In designing and implementing a system of internal control, Management, in its judgment, identifies and considers suitable and relevant points of focus that reflect the entity’s industry, operating, and regulatory environments. Once management has determined which points of focus are suitable and relevant for a particular principle, those points of focus become important considerations when assessing the presence and functioning of a principle.